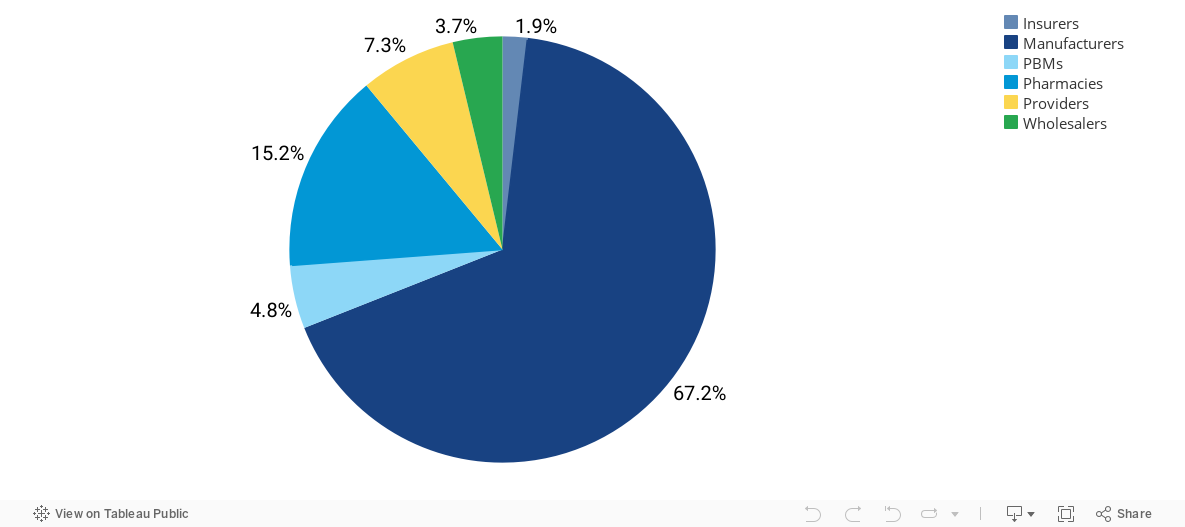

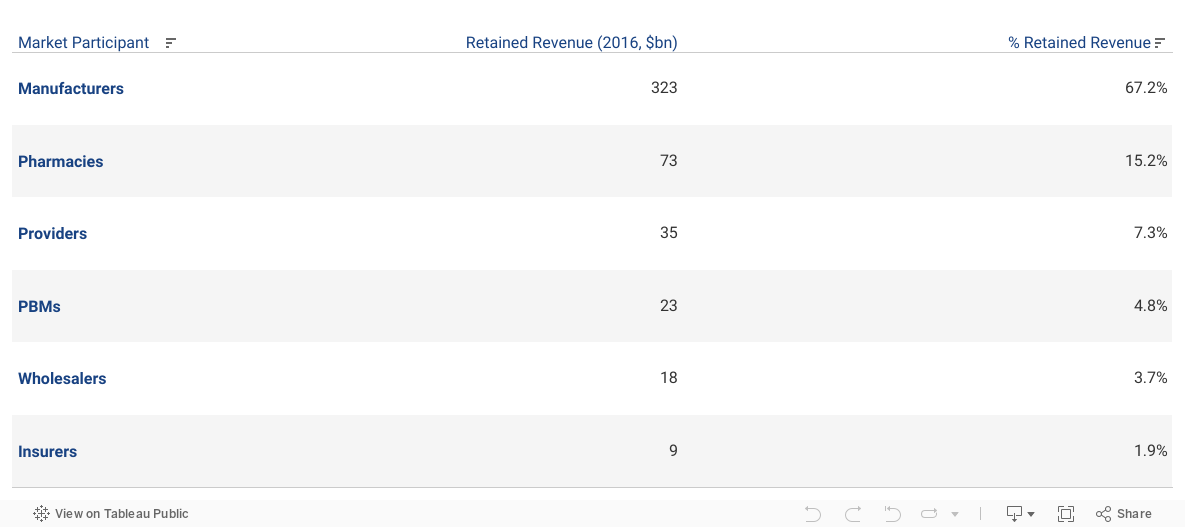

The differential between gross and net revenues reached $187 billion in 2020, with approximately two-thirds of this amount comprised of rebates to third-party payers.1 Rebates are so important to the payer and profits from spread pricing so lucrative for providers that there is strong systemic resistance to recent efforts at reform. Rebates have moved up steadily as a result of the high concentration and market power exerted by the top three PBMs, which process over 75% of all prescription claims.

The entrenched system through which pharmaceutical companies rebate a significant percentage of the reimbursed drug price back to the payer is a structural problem that leads to host of inefficiencies and distorted incentives throughout the supply chain. Payers and PBMs claim rebates keep premiums low. However, recent calls for pricing transparency have led companies to disclose the magnitude of these discounts, underscoring that PBMs and other supply chain intermediaries play an important role in pushing up patients’ drug costs.

Unfortunately, patients, including Part D beneficiaries, typically do not share in these large rebates and steep discounts to the list prices. Coinsurance and cost-sharing in commercial and Part D plans are based on percentages of the pharmacy prices that generally exclude rebates. Since progression through the phases of Medicare Part D is also determined on the basis of these negotiated prices, beneficiaries reach the catastrophic phase more quickly, which also results in higher cost-sharing.

- The average discount for drugs across manufacturers’ portfolios ranged from 45.5% to 50% in 2020, with the difference reflecting the portion of revenues captured by payers (including the government), PBMs, pharmacies and distributors.

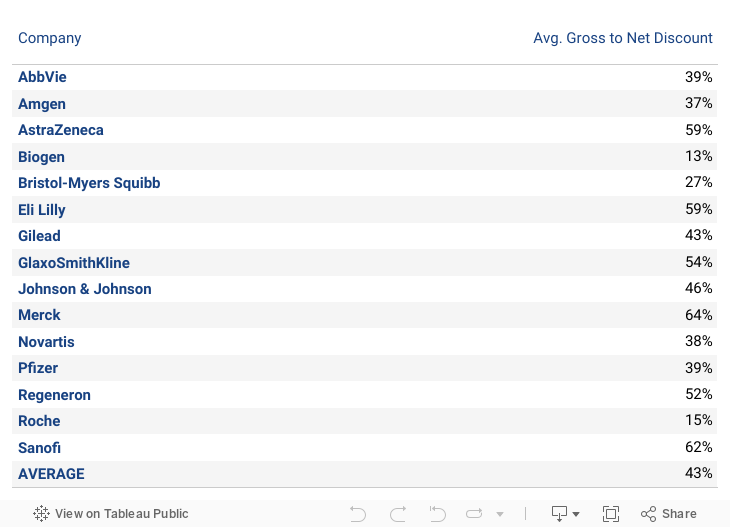

- The average gross-to-net spread for the top 15 companies was 43% in 2019. Although rebates remain the largest component, 340B discounts are a growing factor for certain companies. For example, Merck, Lilly, and Sanofi are near the top due to dominance of diabetes drugs in their portfolios.

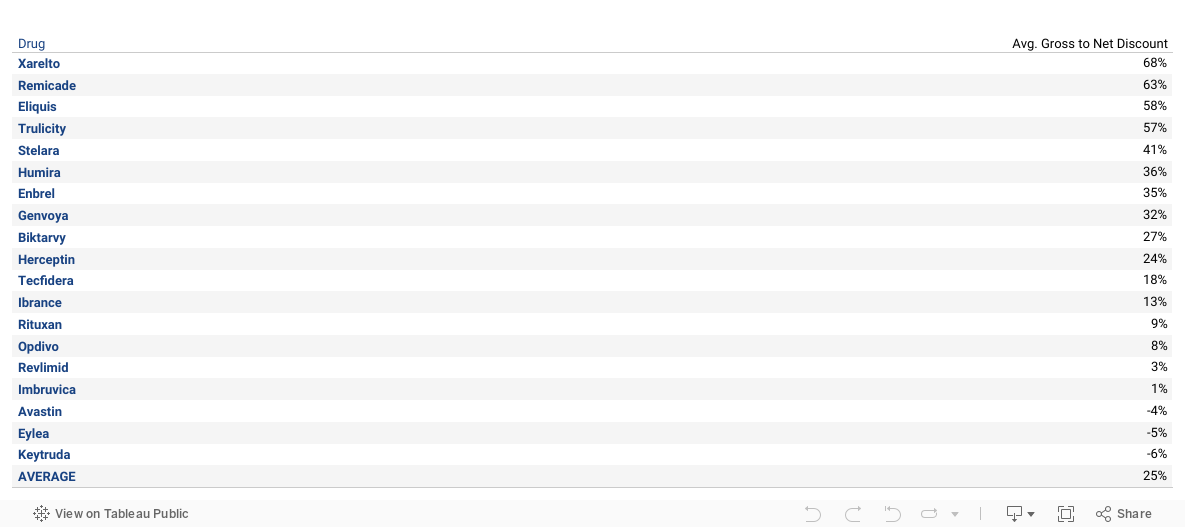

- The differential between the WAC and net price for the 20 largest drugs is 25%, with the 4 largest drugs exceeding 50% discounts.

To see how rebates work within the supply chain, visit our Pricing Tutorials page.